Credit Management Software

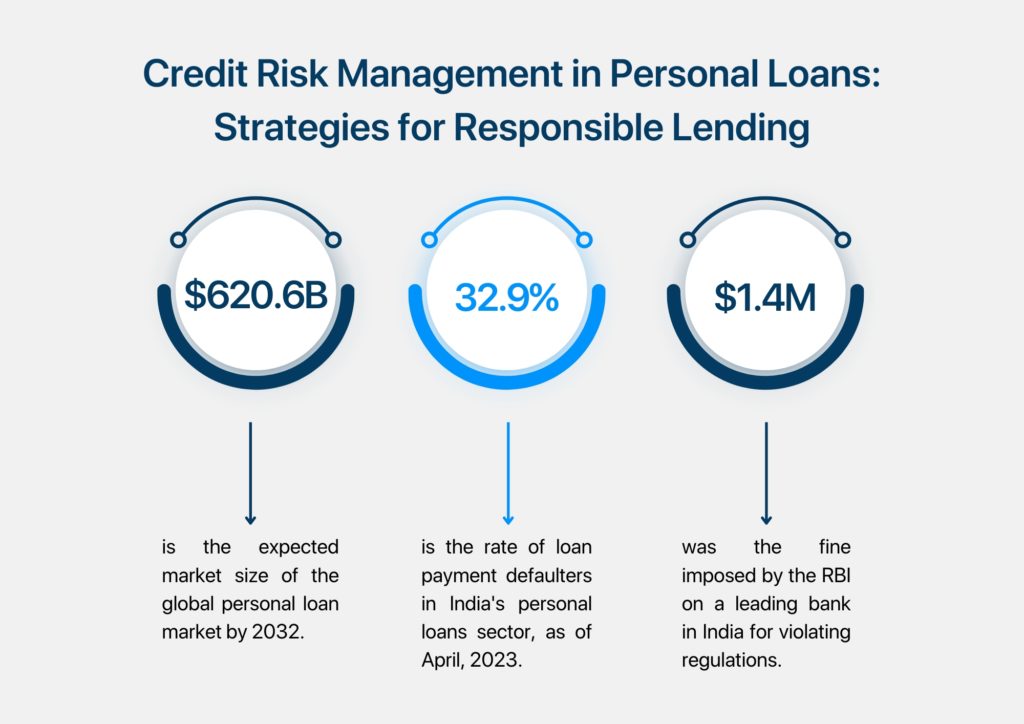

Personal loans are an integral part of lending services, providing borrowers with the money to cover their needs. With the global personal loan market projected to grow from $65.3 billion in 2023 to $620.6 billion by 2032, at a Compound Annual Growth Rate (CAGR) of 32.5%, effective credit risk management is crucial for financial institutions to maintain stability and sustainably grow their lending portfolios. The evolution of technology has given rise to some of the best credit risk management software to minimise risks and maximise profitability for lending institutions.

Credit management software – Credit risk refers to the potential loss a lender may incur if a borrower fails to repay a loan as agreed. It is influenced by various factors, including the borrower’s credit history, income stability, employment status, debt-to-income ratio, and overall financial health. Economic conditions, such as unemployment rates, interest rates, and housing market trends, also affect the credit risk of the borrower.

Strategies for Responsible Lending

Robust Credit Assessment

To determine their creditworthiness, lenders should analyse the borrower’s credit report, income documentation, employment history, and debt obligations. Utilising credit scoring models and risk analytics can help evaluate the likelihood of default accurately. In India alone, according to TransUnion Cibil, wilful defaulters rose to ₹353,874 crore (42.7M USD) in March 2023 from ₹304,063 crore (36.67M USD) the previous year. Among these, 77% are associated with nationalized banks, underscoring the necessity for a robust credit risk assessment system. Corestrat’s Digital Lending Automation (DLA), powered by AI and ML, is one of the best credit risk management software solutions that evaluates borrower creditworthiness from credit history and personal data, automating loan decisions for improved risk management whilst maximizing lending margins across customer segments.

Monitoring and Early Warning Systems

Implementing robust monitoring mechanisms and early warning systems enables lenders to identify signs of financial distress among borrowers promptly. credit management software – Regularly tracking repayment behaviour, changes in credit scores, and economic indicators allows lenders to take proactive measures, such as offering loan modifications or restructuring, to prevent defaults. DLA features a customer management system, enabling lending institutions to monitor borrower behaviour in real-time and swiftly address any red flags to mitigate credit risks.

Setting Appropriate Loan Terms

Matching the loan terms with the borrower’s financial capability is critical for responsible lending. Lenders should offer loan amounts, interest rates, and repayment schedules that borrowers can comfortably afford. The percentage of unsecured loan payment defaulters in India’s personal loans sector has risen to 32.9% as of April 21, 2023, up from 31.4% a year earlier. credit management software – Finding the right balance between mitigating credit risk and enabling access to credit is critical for promoting financial inclusion while protecting against defaults.

Compliance with Regulatory Standards

Lending institutions must adhere to the regulatory compliances set by regulatory bodies, such as the central bank of the country (e.g., RBI for India), to guarantee fair treatment of borrowers and effective credit risk management for the institution. Institutions risk substantial fines for non-compliance with regulations, as evidenced by ICICI’s ₹12.19 crore penalty in India for violating RBI regulations. It’s crucial for lending institutions to continuously monitor the evolving regulatory landscape and stay updated on regulatory changes. This proactive approach helps prevent lending to inappropriate individuals and mitigates the risk of financial and reputational harm. DLA simplifies the process of monitoring and staying updated on regulatory changes, freeing lending institutions to focus on more critical tasks while entrusting routine regulatory duties to the credit management software.

Conclusion

The role of credit risk management is significant in promoting responsible lending practices in personal loans. By implementing robust credit assessment processes, setting appropriate loan terms, diversifying portfolios, monitoring borrower behaviour, and complying with regulatory standards, lending institutions can mitigate credit risk while facilitating access to credit for consumers. Embracing responsible lending principles not only safeguards the financial health of lenders but also fosters trust and sustainability in the lending ecosystem.

The Digital Lending Automation (DLA), Corestrat’s premier lending automation platform, harnesses the power of AI and ML to digitise and automate the lending process. Renowned for its superior credit risk management capabilities, it thoroughly evaluates borrower applications and details, enabling lending institutions to manage risks efficiently.

Learn more about automating and digitising the lending process while having an efficient credit risk management system within your institution: